45 duration of a coupon bond

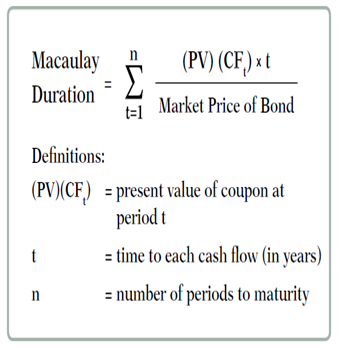

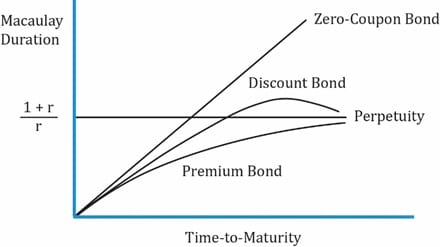

Duration - Definition, Types (Macaulay, Modified, Effective) It is a measure of the time required for an investor to be repaid the bond's price by the bond's total cash flows. The Macaulay duration is measured in units of time (e.g., years). The Macaulay duration for coupon-paying bonds is always lower than the bond's time to maturity. For zero-coupon bonds, the duration equals the time to maturity. Macaulay Duration - Investopedia 29.09.2022 · Macaulay Duration: The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the ...

Dollar Duration - Overview, Bond Risks, and Formulas Dollar Duration. The change in the price of the bond for every 100 bps (basis points) of change in the interest rate. Written by CFI Team. Updated August 31, 2021. ... It means that as interest rates fall, bond coupon rates increase. Short-term bonds are less sensitive to interest changes, while a 20-year long-term bond may be more sensitive to ...

Duration of a coupon bond

How to Calculate Bond Duration - wikiHow To calculate bond duration, you will need to know the number of coupon payments made by the bond. This will depend on the maturity of the bond, which represents the "life" of the bond, between the purchase and maturity (when the face value is paid to the bondholder). Dollar Duration Definition - Investopedia Remember, 0.01 is equivalent to 1 percent, which is often denoted as 100 basis points (bps). To calculate the dollar duration of a bond you need to know its duration, the current interest rate, and... exploringfinance.com › bond-duration-calculatorBond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator:

Duration of a coupon bond. What is the duration of a bond? and How to Calculate It? Duration of a Bond. The duration of a bond does not represent the duration for which an investor holds a bond. Instead, it refers to the relationship between the price of a bond and interest rates of the bond after considering its different characteristics such as … Zero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total … Duration | Definition & Examples | InvestingAnswers The lower the coupon, the longer the duration (and volatility). Zero-coupon bonds - which have only one cash flow - have durations equal to their maturities. 2. Maturity. The longer a bond's maturity, the greater its duration and volatility. Duration changes every time a bond makes a coupon payment, shortening as the bond nears maturity. dqydj.com › bond-duration-calculatorBond Duration Calculator – Macaulay and Modified Duration Coupon Payment Frequency - How often the bond pays interest per year. Calculator Outputs Yield to Maturity (%): The yield until the bond matures, as computed by the tool. See the yield to maturity calculator for more details. Macaulay Duration (Years) - The weighted average time (in years) for the bond's cash flows to pay out.

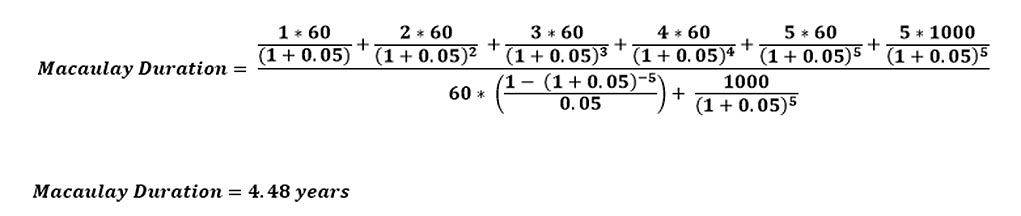

Duration and Convexity to Measure Bond Risk - Investopedia However, for zero-coupon bonds, duration equals time to maturity, regardless of the yield to maturity. The duration of level perpetuity is (1 + y) / y. For example, at a 10% yield, the duration of... Understanding the Relationship Between Coupon Rates and Duration A high coupon rate bond provides more cash flow than a low coupon rate bond. Accordingly, a high coupon rate bond has a lower duration that a low coupon bond. For example, if I purchase a zero-coupon bond on its issue date the bond will have a duration of 30 years - no cash flow until the bond matures. Bond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. … › terms › dDuration Definition and Its Use in Fixed Income Investing Time to maturity and a bond's coupon rate are two factors that can affect a bond's duration. Macaulay duration estimates how many years it will take for an investor to be repaid the bond's price by...

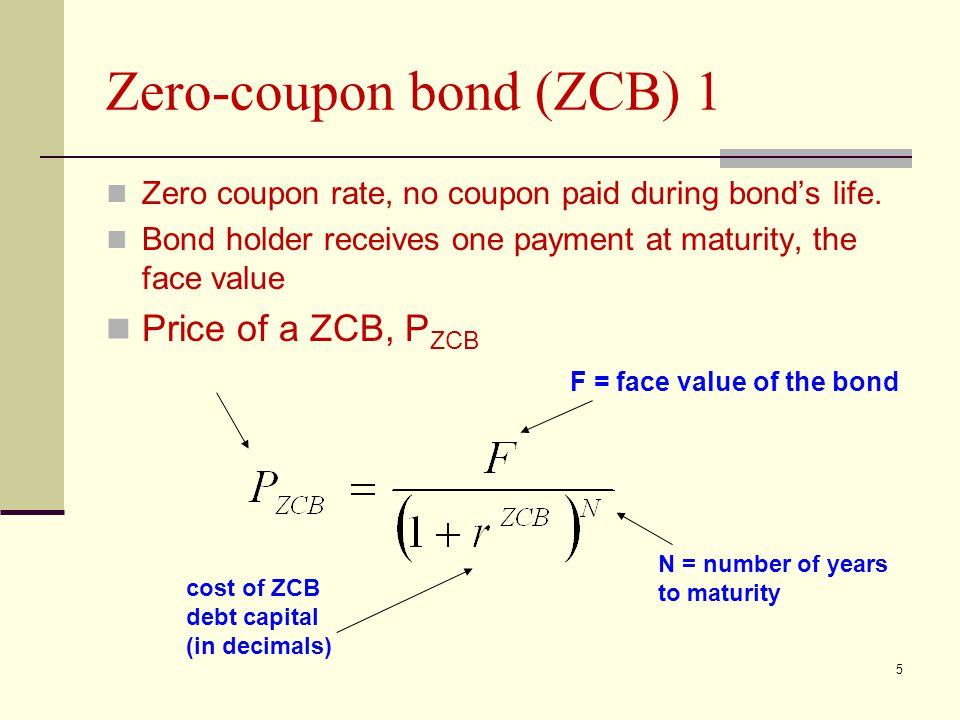

Bond Convexity Calculator: Estimate a Bond's Yield Sensitivity In the bond duration example, we computed the duration for a made up bond. Let's use the same example and compute convexity: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5%; Years to Maturity: 3; Coupon Payouts: One a Year; Duration, Modified Duration: 2.856, 2.682 (Note: this calculation is in the bond ... Duration Formula (Excel Examples) | Calculate Duration of Bond Calculate the bond duration for the following annual coupon rate: (a) 8% (b) 6% (c) 4% Given, M = $100,000 n = 4 r = 10% Calculation for Coupon Rate of 8% Coupon payment (C)= 8% * $100,000 = $8,000 The denominator or the price of the bond is calculated using the formula as, Bond price = 88,196.16 Duration Definition and Its Use in Fixed Income Investing - Investopedia 01.09.2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... › zero-coupon-bondZero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far.

Macaulay Duration of a Semi annual coupon bond

Duration: Understanding the Relationship Between Bond Prices and ... In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date. The larger the coupon, the shorter the duration number becomes.

:max_bytes(150000):strip_icc()/Convexity22-0370dbde8e1c4a958bff8b670bf8bf5c.png)

Convexity Definition

Coupon Bond - Guide, Examples, How Coupon Bonds Work Let's imagine that Apple Inc. issued a new four-year bond with a face value of $100 and an annual coupon rate of 5% of the bond's face value. In this case, Apple will pay $5 in annual interest to investors for every bond purchased. After four years, on the bond's maturity date, Apple will make its last coupon payment.

Solved You are managing a portfolio of $1 million. Your ...

Convexity of a Bond | Formula | Duration | Calculation While the duration of the zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a discount to its par value and does not pay periodic interest. In other words, the annual implied interest payment is included into the face value of the bond, …

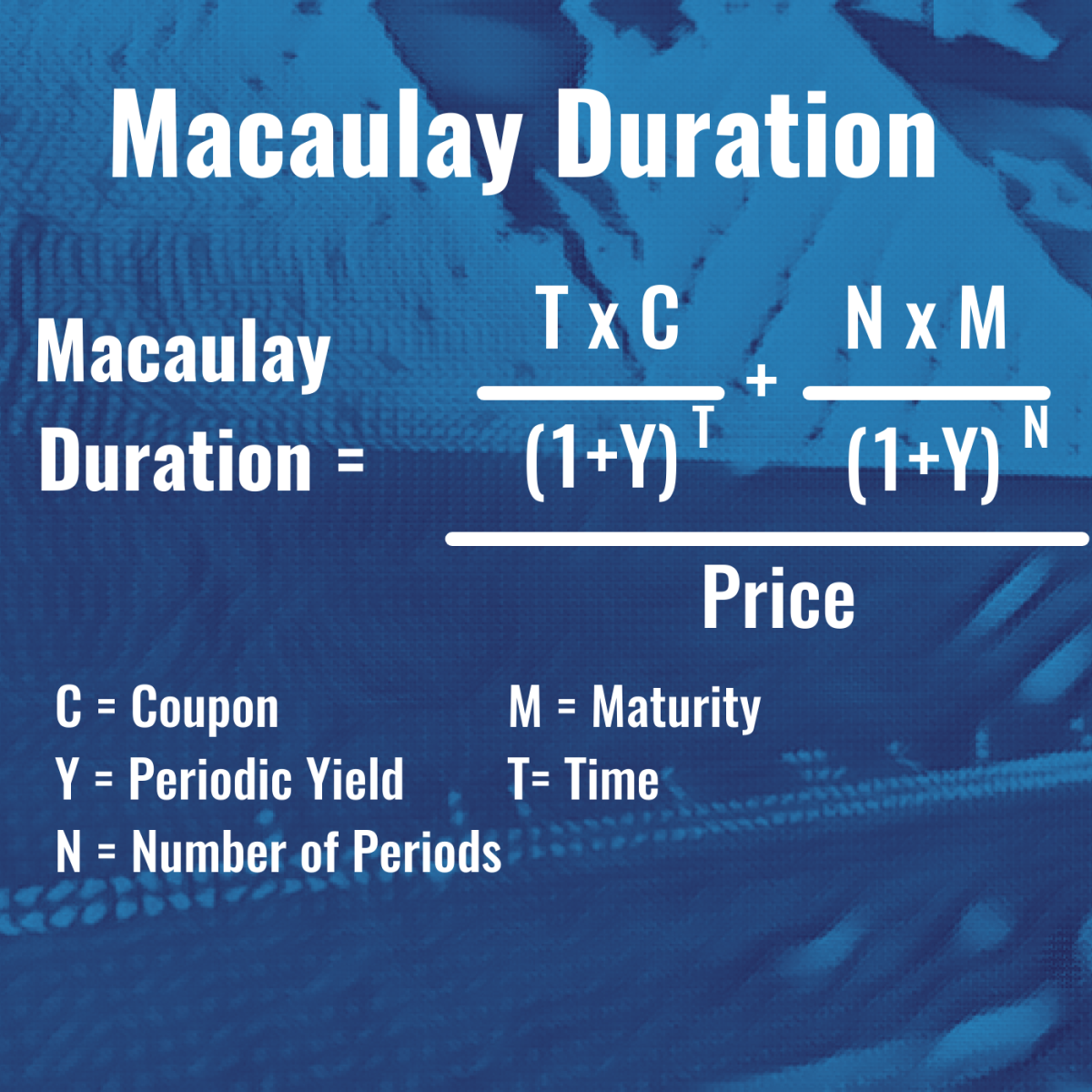

Macaulay Duration

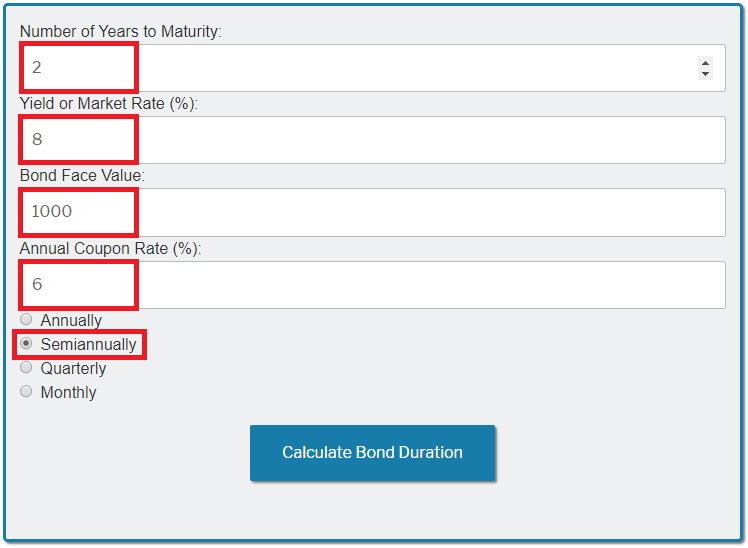

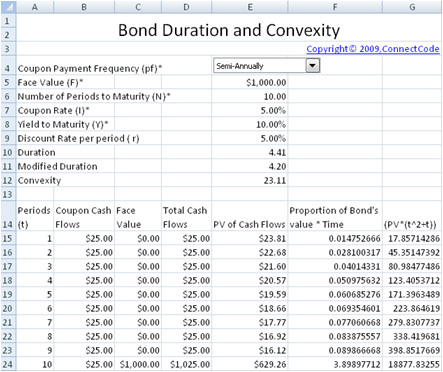

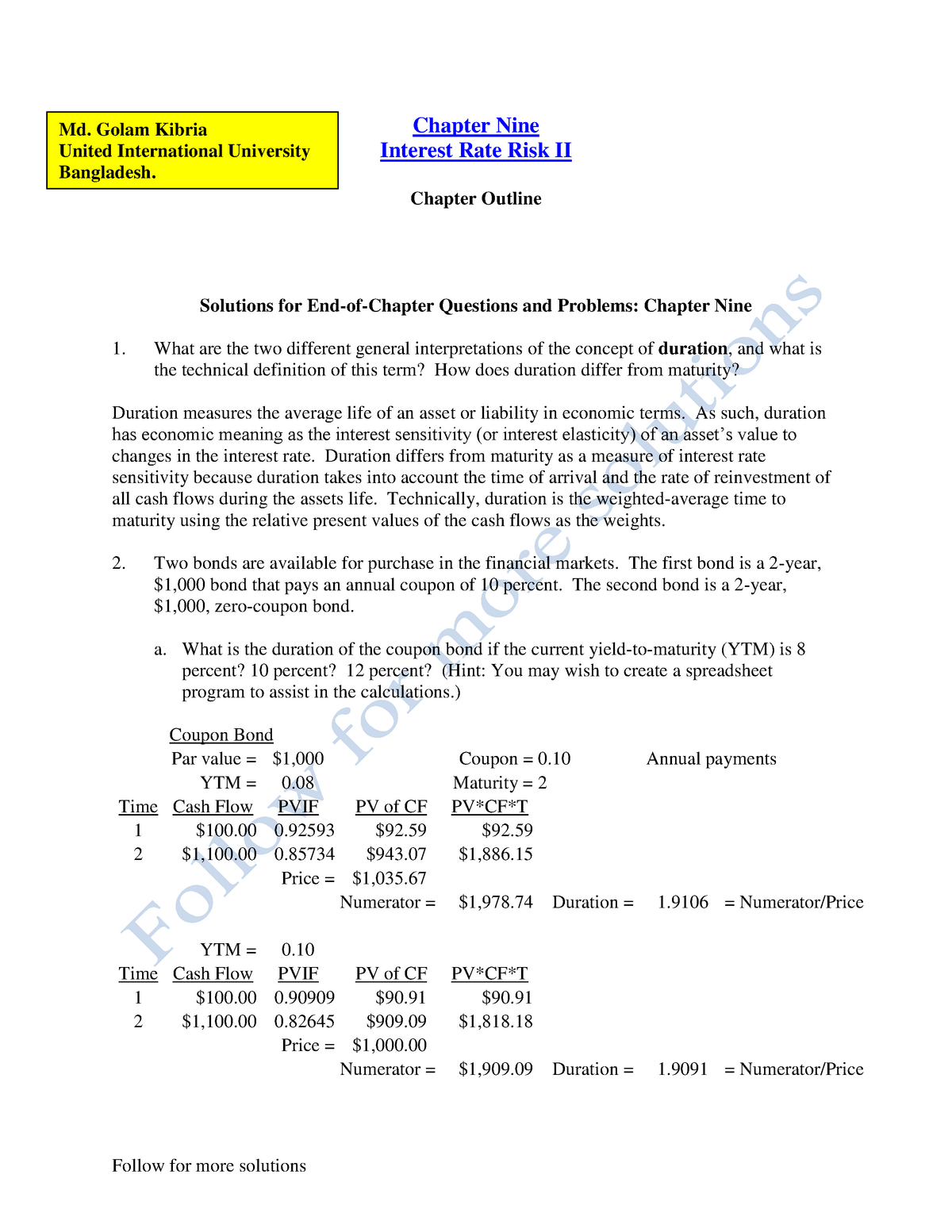

How to Calculate the Bond Duration (example included) PV = Bond price = 963.7 FV = Bond face value = 1000 C = Coupon rate = 6% or 0.06 Additionally, since the bond matures in 2 years, then for semiannual bond you'll have a total of 4 coupon payments (one payment every 6 months), such that: t1 = 0.5 years t2 = 1 years t3 = 1.5 years t4 = tn = 2 years

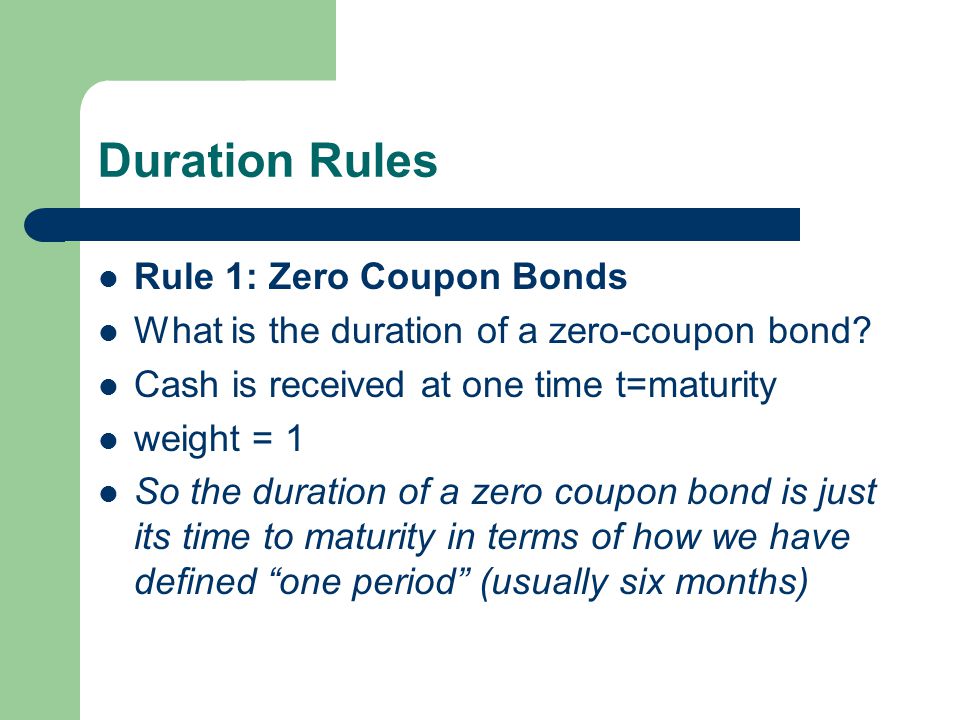

Interest-Rate Risk II. Duration Rules Rule 1: Zero Coupon ...

dqydj.com › bond-convexity-calculatorBond Convexity Calculator: Estimate a Bond's Yield ... - DQYDJ In the bond duration example, we computed the duration for a made up bond. Let's use the same example and compute convexity: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5%; Years to Maturity: 3; Coupon Payouts: One a Year; Duration, Modified Duration: 2.856, 2.682 (Note: this calculation is in the bond ...

![Duration and Convexity [Concepts Series] | by Byrne Hobart ...](https://miro.medium.com/max/934/1*sId1I-O1GXScie24NpUXyQ.png)

Duration and Convexity [Concepts Series] | by Byrne Hobart ...

The dynamics of bond duration and rising rates | Vanguard 18.11.2021 · Your investment horizon matters. Rising interest rates can be good for bond investors if their investment horizon is long enough. Figure 1 shows the effect of the investment horizon on a hypothetical investment in a bond maturing in 15 years that pays a coupon of 0.9% annually when interest rates are at 2%. The bond’s weighted average Macaulay duration is 14 …

Bond Valuation and Risk - ppt video online download

› convexity-of-a-bondConvexity of a Bond | Formula | Duration | Calculation For a Bond of Face Value USD1,000 with a semi-annual coupon of 8.0% and a yield of 10% and 6 years to maturity and a present price of 911.37, the duration is 4.82 years, the modified duration is 4.59, and the calculation for Convexity would be:

Duration & Convexity - Fixed Income Bond Basics | Raymond James

› duration-bondWhat is the duration of a bond? and How to Calculate It? Usually, the duration of a bond shows the number of years in which an investor can recover the present value of the cash flows of a bond. It can also represent a percentage that is a measure of how sensitive the value of the bond is to changes in interest rates. The duration of a bond is simple to understand.

Under the Hood: What You Need to Know About Bond Duration and ...

The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and...

Macaulay, Modified, and Effective Durations | CFA Program ...

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Advanced Bond Concepts: Duration | The Financial Engineer

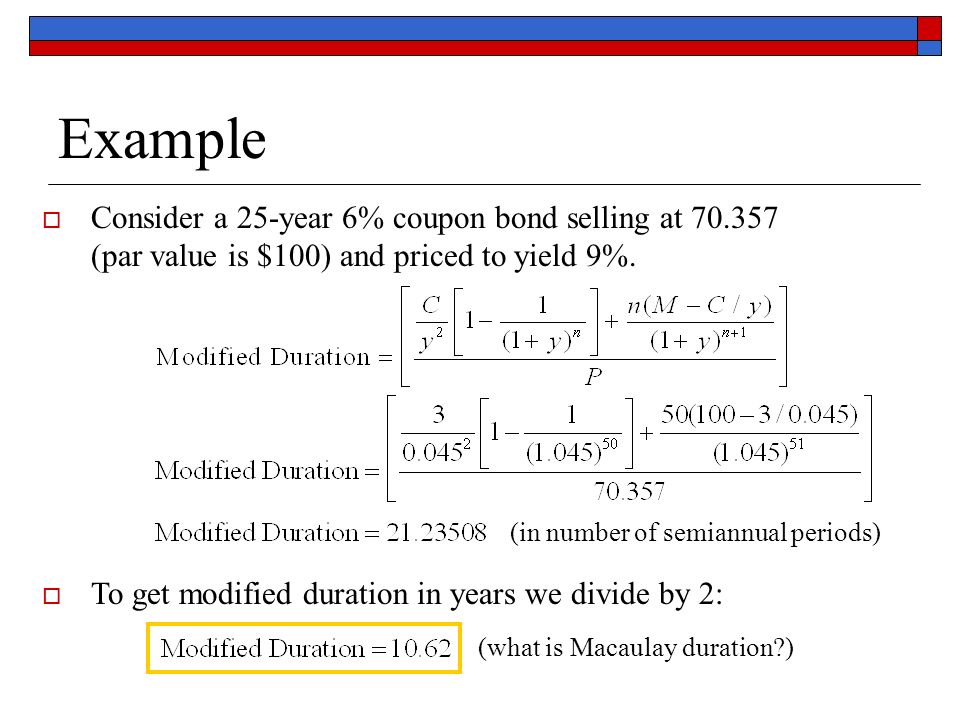

Bond duration - Wikipedia For example, a standard ten-year coupon bond will have a Macaulay duration of somewhat but not dramatically less than 10 years and from this, we can infer that the modified duration (price sensitivity) will also be somewhat but not dramatically less than 10%.

Bond Duration - Retirement Researcher

Coupon Bond - Investopedia The coupon rate is calculated by taking the sum of all the coupons paid per year and dividing it with the bond's face value. Real-World Example of a Coupon Bond If an investor purchases a $1,000...

Bond Duration Calculator - Exploring Finance

Bond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

What is the duration of a two-year bond that pays an annual ...

Understanding bond duration - Education | BlackRock Conversely, if a bond has a duration of five years and interest rates fall by 1%, the bond's price will increase by approximately 5%. Understanding duration is particularly important for those who are planning on selling their bonds prior to maturity. If you purchase a 10-year bond that yields 4% for $1,000, you will still receive $40 dollars ...

Bond Duration | Formula | Excel | Example

exploringfinance.com › bond-duration-calculatorBond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator:

fixed income - How can a deep discount bond with a longer ...

Dollar Duration Definition - Investopedia Remember, 0.01 is equivalent to 1 percent, which is often denoted as 100 basis points (bps). To calculate the dollar duration of a bond you need to know its duration, the current interest rate, and...

What Is Duration of a Bond? - TheStreet Definition - TheStreet

How to Calculate Bond Duration - wikiHow To calculate bond duration, you will need to know the number of coupon payments made by the bond. This will depend on the maturity of the bond, which represents the "life" of the bond, between the purchase and maturity (when the face value is paid to the bondholder).

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

mathematics - Modified Durations of Different Noncallable ...

Bond Duration | Formula | Excel | Example

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

:max_bytes(150000):strip_icc()/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Duration and Convexity to Measure Bond Risk

FRM: Dollar duration of zero coupon bond

Free Bond Duration and Convexity Spreadsheet

:max_bytes(150000):strip_icc()/dotdash_Final_Duration_Aug_2020-02-a79edb63b9264dc9a76ee587240a27ea.jpg)

Duration Definition and Its Use in Fixed Income Investing

Bond Modified Duration in R | R-bloggers

Bond Economics: Primer: Low Yields and Duration

WWWFinance - Bond Valuation: Campbell R. Harvey

Duration and Convexity, with Illustrations and Formulas

Calculation of Duration and Convexity (5-year, $100 face ...

Duration Analysis

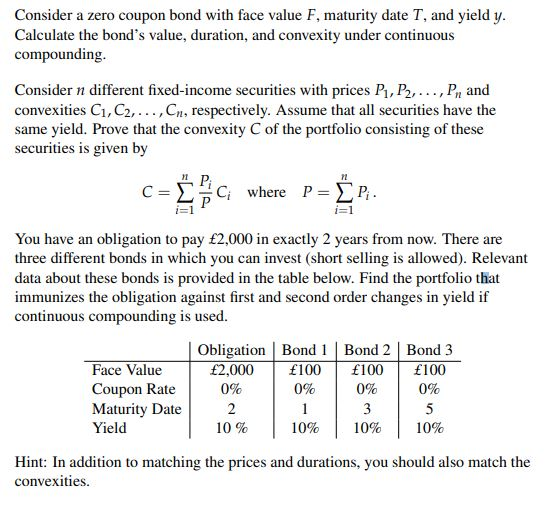

Consider a zero coupon bond with face value F, | Chegg.com

Macaulay Duration

Making sense of duration sensitivity | Fidelity UAE

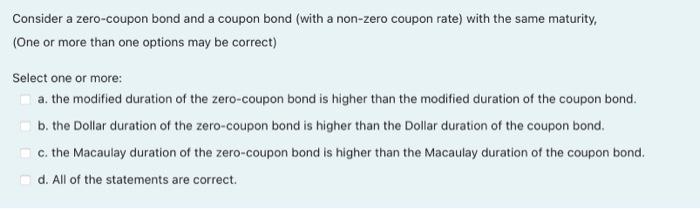

Solved Consider a zero-coupon bond and a coupon bond (with a ...

Maximum duration of a coupon bond - Bogleheads.org

What is the duration of a 10-year treasury bond? - Quora

What Is Duration of a Bond? - TheStreet Definition - TheStreet

Chap009 duration gap model - Md. Golam Kibria United ...

Duration

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

Understanding Fixed-Income Risk and Return | IFT World

Macaulay Duration Formula | Example with Excel Template

Premium Bonds 101 | Breckinridge Capital Advisors

Post a Comment for "45 duration of a coupon bond"