38 zero coupon bond accrued interest

r/bonds - zero coupon tbills. I am new to tbills, I have started buying ... 6.3K subscribers in the bonds community. The biggest community on Reddit related to bonds. ... I have started buying tbills but have been choosing zero coupon. Is there an advantage to buying non-0 coupon tbills, comments sorted by Best Top New Controversial Q&A Add a Comment . ... r/bonds • Accrued Interest. r/bonds ... › zero-coupon-bondZero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far.

ICE BofA US Corporate Index Effective Yield (BAMLC0A0CMEY) Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US domestic bond markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date.

Zero coupon bond accrued interest

Search Results | FRED | St. Louis Fed This is called a zero coupon bond. Because high quality zero coupon bonds are not generally available, the HQM methodology computes the spot rates so as to make them consistent with the yields on other high quality bonds. The HQM yield curve uses data from a set of high quality corporate bonds rated AAA, AA, or A that accurately represent the ... ICE BofA Emerging Markets Corporate Plus Index Total Return ... - FRED Accrued interest for US mortgage pass-through and US structured products is calculated assuming same-day settlement. Cash flows from bond payments that are received during the month are retained in the index until the end of the month and then are removed as part of the rebalancing. ICE BofA US Corporate Index Total Return Index Value Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US domestic bond markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date.

Zero coupon bond accrued interest. Bonds of Mass Destruction - The Last Bear Standing Let's look at the price instead. This particular bond was issued in October 2020 with a coupon of 0.50%. Allegedly sane, sophisticated investors lent the U.K. government money at a fixed rate of 0.50% for forty years. While this sounds like a boring investment, it is an extraordinarily risky bet on interest rates. ICE BofA Euro High Yield Index Semi-Annual Yield to Worst ... Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and euro domestic markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. en.wikipedia.org › wiki › Dirty_priceDirty price - Wikipedia To avoid the impact of the next coupon payment on the price of a bond, this cash flow is excluded from the price of the bond and is called the accrued interest. In finance , the dirty price is the price of a bond including any interest that has accrued since issue of the most recent coupon payment. › terms › iImputed Interest Definition - Investopedia Apr 25, 2022 · Imputed interest is used by the Internal Revenue Service (IRS) as a means of collecting tax revenues on loans or securities that pay little or no interest. Imputed interest is important for ...

ICE BofA US High Yield Index Effective Yield - St. Louis Fed Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US domestic bond markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. Chile Government Bonds - Yields Curve The Chile 10Y Government Bond has a 7.120% yield. 10 Years vs 2 Years bond spread is -259 bp. Yield Curve is inverted in Long-Term vs Short-Term Maturities. Central Bank Rate is 10.75% (last modification in September 2022). The Chile credit rating is A, according to Standard & Poor's agency. Some bonds on secondary market are essentially "Zero-Coupon" bonds With yields rising, many older bonds are selling at a discount but their coupon can be relatively low (e.g 0.9%). With the discounted purchase price the YTW can be much higher (e.g. 3.8%). But the YTW takes into account the fact that you purchased the bond at a cost of less than $1000, and when it's redeemed you will receive $1000. Yield to Call Formula & Examples | How to Calculate Yield to Call ... The bonds are callable at a strike price of $1,050 with a premium of $60 above par and any accrued interest. The bonds cannot be called for the first two years. In this example, the coupon rate is...

How to Calculate the Issue Price of a Bond in Excel Then, if we want to calculate a zero coupon bond price, then we have to set the coupon rate to 0%. The zero-coupon bond can be defined as a bond that doesn't pay interest during the life of that bond. The investor buys the zero-coupon bond at a deep interest from its face value whereas, after maturity, the investor will sell it at its face ... Bonds vs Bond-ETFs : r/bonds - reddit.com There are 2 types of bonds, government bonds, which generally are considered to have zero (or near zero) default risk (but have other risks, such as interest rate, inflation and duration risks to name the most common). Corporate bonds are not openly traded, but are privately traded, so you can't just buy one. How To Invest In Treasury Bills - KXLY Bondholders receive interest payments every six months and are paid the face value of the bond at maturity. Treasury Notes. These intermediate-term securities offer maturities of two to 10 years. › terms › bWhat Is Bond Yield? - Investopedia May 31, 2022 · Bond Yield: A bond yield is the amount of return an investor realizes on a bond. Several types of bond yields exist, including nominal yield which is the interest paid divided by the face value of ...

Problems and Solutions

ICE BofA US Corporate Index Option-Adjusted Spread Each security must have greater than 1 year of remaining maturity, a fixed coupon schedule, and a minimum amount outstanding of $250 million. Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US

Calculation of the price of a bond

ICE BofA US High Yield Index Option-Adjusted Spread Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US domestic bond markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date.

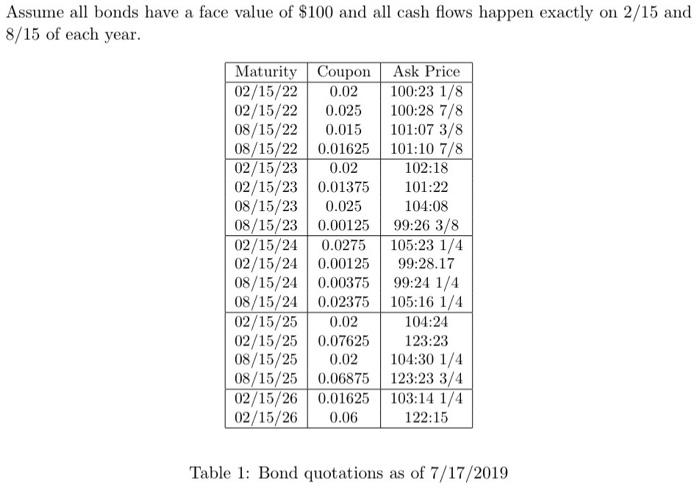

1) Adjust the bond price quotes in Table 1 for | Chegg.com

› bond-formulaBond Formula | How to Calculate a Bond | Examples with Excel ... Let us take the example of another bond issue by SDF Inc. that will pay semi-annual coupons. The bonds have a face value of $1,000 and a coupon rate of 6% with maturity tenure of 10 years. Calculate the price of each coupon bond issued by SDF Inc. if the YTM based on current market trends is 4%.

Zero Coupon Bonds - Financial Edge

dqydj.com › bond-convexity-calculatorBond Convexity Calculator: Estimate a Bond's Yield ... - DQYDJ Bond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is:

What are zero-coupon bonds?

Bonds- Price, YTM, Duration - BrainMass US Treasury Notes Coupon Yield to Maturity Zero coupon rate 1 Year 3.25% 3% 3% 2 Year 3.80% 3.25% 3 Year 4.5% 3.5% 4 Year 5% 4% 5 Year 6% 4.5% You can assume that coupon payments are annual and that you are pricing on a coupon day (no accrued interest) and you may ignore basis conventions.

Untitled

GPW Benchmark - Index factsheet TBSP.Index is a total return index which includes the bond price performance, accrued interest, and revenue from reinvested coupons. The index portfolio comprises zero coupon bonds and fixed rate bonds denominated in Polish zlotys. The index is calculated on the basis of bond prices set on TBSP fixing sessions.

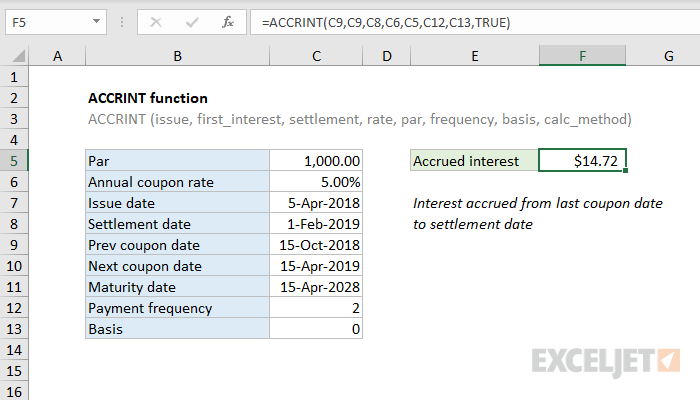

How to use the Excel ACCRINT function | Exceljet

Investing in Bonds - FAIRWINDS Credit Union No interest is paid, but at maturity you receive the face value of the bond. For example, you pay $600 for a 5-year, $1,000 zero-coupon bond. At the end of 5 years, you receive $1,000. Corporate bonds have maturity dates ranging from one day to 40 years or more and generally make fixed interest payments every six months. U.S. government securities

14.1: Determining the Value of a Bond - Mathematics LibreTexts

Bond Noob question : r/bonds - reddit.com I am new to bonds. I have a question, I am looking at UNITED STATES TREAS BILLS ZERO CPN 0.00000% 01/24/2023 (yield 3.58, yield to worst 3.529, yield to maturity 3.529, 3rd party price 98.868, maturity date 01/24/2023). Does this mean that on a $100k the bond will pay $3529 after 3 months guaranteed?

Accrued Interest Formula | Calculator (Examples with Excel ...

en.wikipedia.org › wiki › Current_yieldCurrent yield - Wikipedia Example. The current yield of a bond with a face value (F) of $100 and a coupon rate (r) of 5.00% that is selling at $95.00 (clean; not including accrued interest) (P) is calculated as follows.

Lecture 09: Multi-period Model Fixed Income, Futures, Swaps

ICE BofA US Corporate Index Total Return Index Value Original issue zero coupon bonds, "global" securities (debt issued simultaneously in the eurobond and US domestic bond markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date.

Zero-Coupon Bond | AwesomeFinTech Blog

ICE BofA Emerging Markets Corporate Plus Index Total Return ... - FRED Accrued interest for US mortgage pass-through and US structured products is calculated assuming same-day settlement. Cash flows from bond payments that are received during the month are retained in the index until the end of the month and then are removed as part of the rebalancing.

Q&A on TIPS | Treasury Inflation-Protected Securities

Search Results | FRED | St. Louis Fed This is called a zero coupon bond. Because high quality zero coupon bonds are not generally available, the HQM methodology computes the spot rates so as to make them consistent with the yields on other high quality bonds. The HQM yield curve uses data from a set of high quality corporate bonds rated AAA, AA, or A that accurately represent the ...

Lab | Points of interest and pitfalls

Bond Pricing and Accrued Interest, Illustrated with Examples

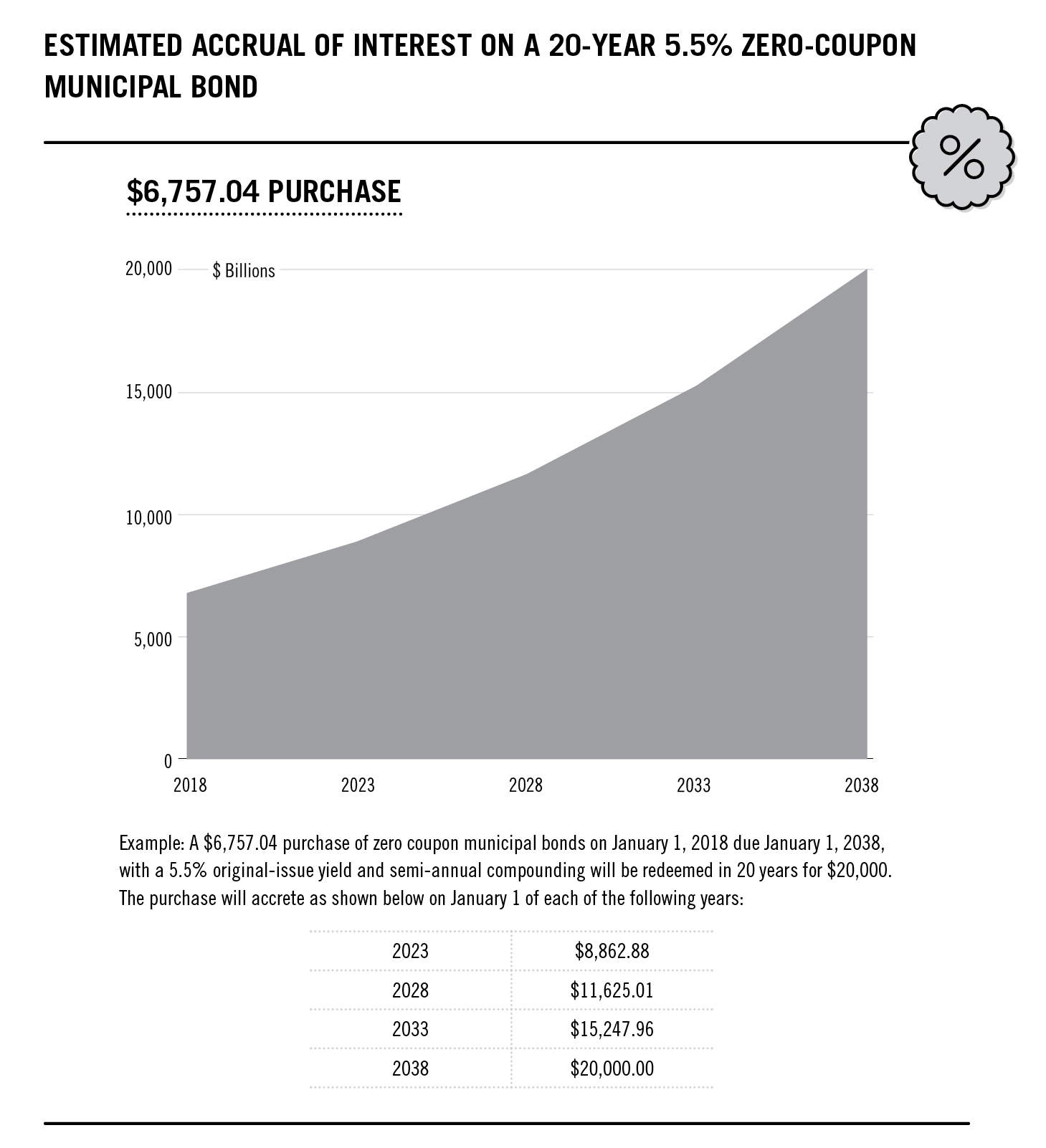

Investor's Guide to Zero-Coupon Municipal Bonds | Project ...

Zero Coupon Bonds Chapter 7 Tools & Techniques of Investment ...

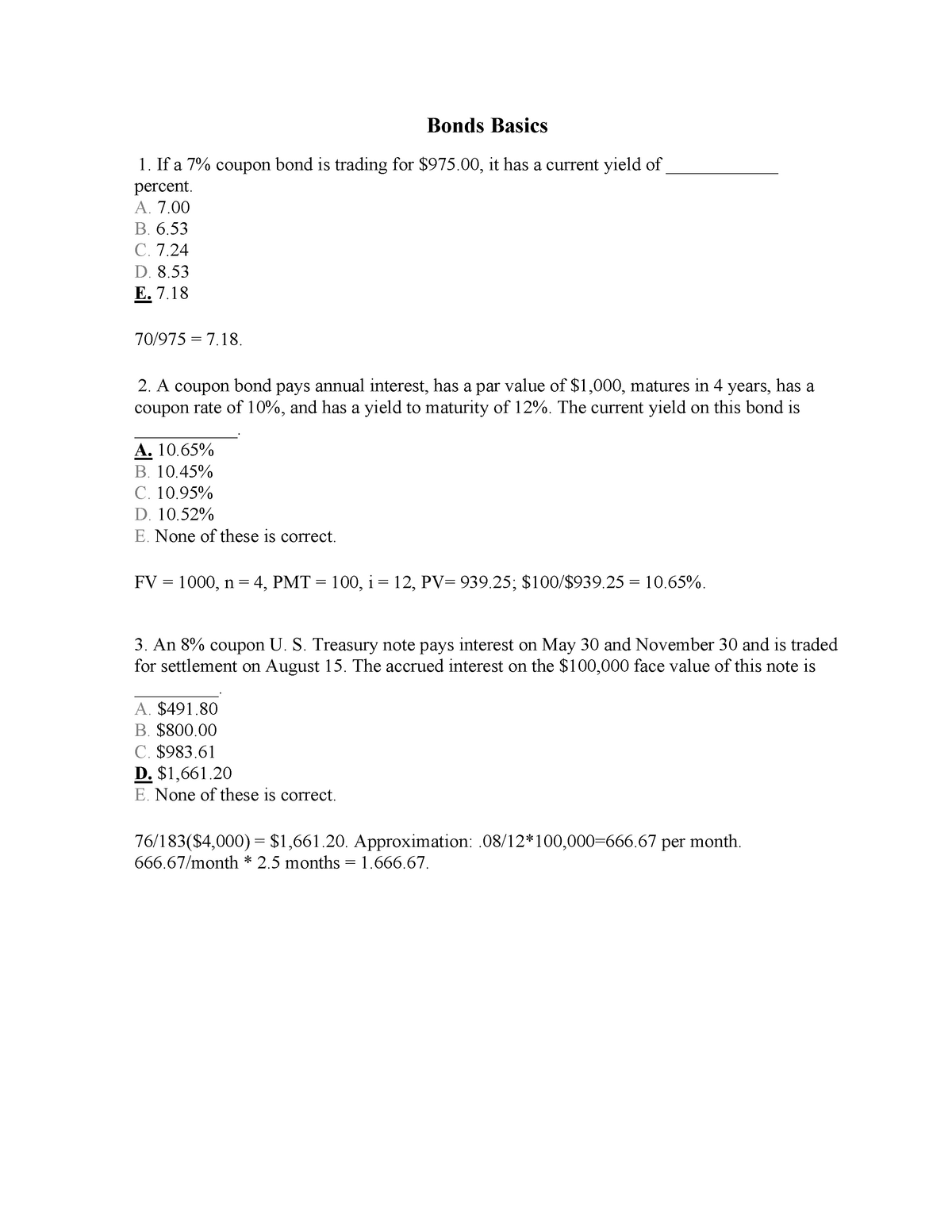

Bonds - Basics - Bonds Basics If a 7% coupon bond is trading ...

Zero Coupon Municipal Bonds: Tax Treatment - TheStreet

Accrued Interest Calculator 【Calculate Cost of Interest】

Bond Prices and Yields Chapter 14. Face or par value Coupon ...

What is the yield to maturity (YTM) of a zero coupon bond ...

Zero-coupon yield curves: technical documentation, BIS Papers ...

Flat Price, Accrued Interest, Full Price - Bond | CFA Level 1 ...

EXCEL Duration Calculation between Coupon Payments ...

Deep Discount bonds and Zero Coupon Bonds - The Fixed Income

Zero-Coupon Bond - an overview | ScienceDirect Topics

What Are Zero Coupon Bonds? - Annuity.com

A 7% coupon rate bond has a face value of $1,000, pays ...

How to Buy Zero Coupon Bonds

Bond Prices and Yields Chapter 14. Face or par value Coupon ...

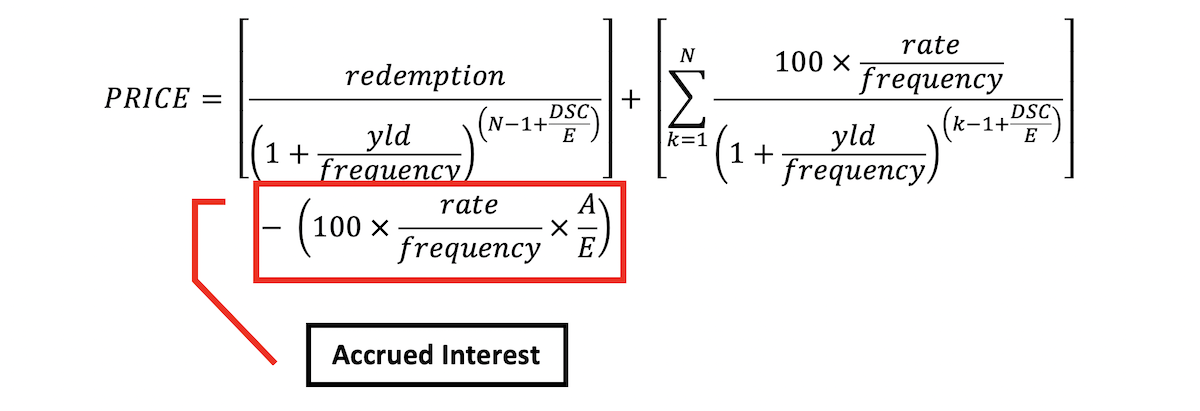

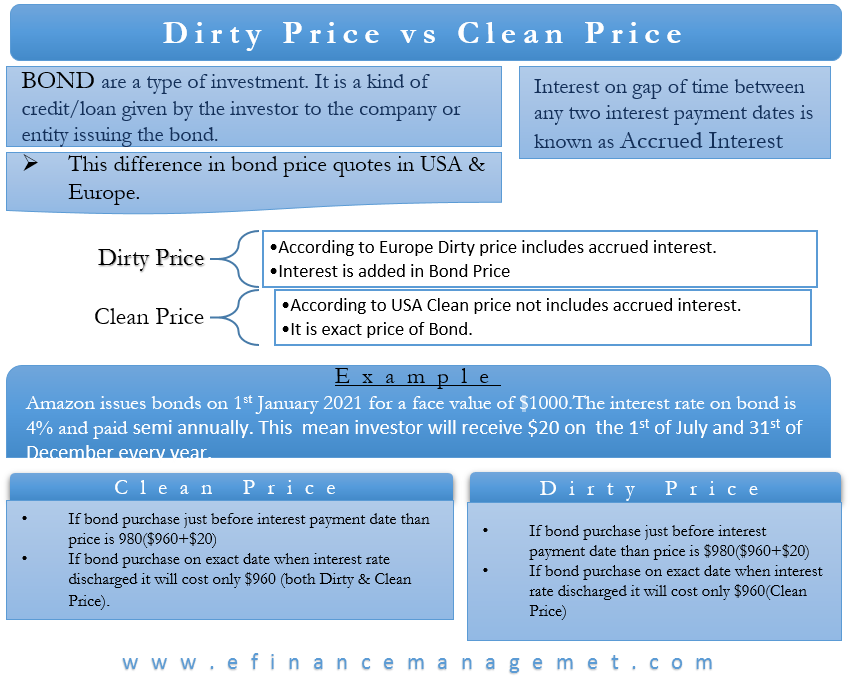

Dirty Price vs Clean Price | Concept | Difference ...

Is Accrued Interest on a Tax Free Bond Deductible?

Bond pricing - Bogleheads

Bond pricing - Bogleheads

Corporate Finance (Berk/DeMarzo)

Duration and Convexity in Bond market

Kynex Dividend Assumptions

Portfolio Duration and its Limitations | CFA Level 1 ...

Post a Comment for "38 zero coupon bond accrued interest"